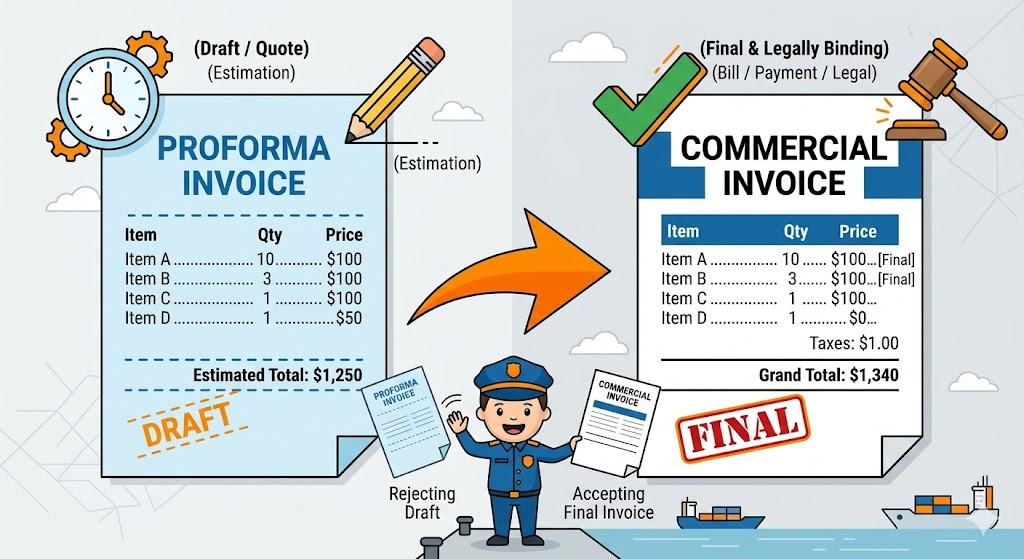

A proforma invoice is a preliminary quotation used before shipment. A commercial invoice is the final sales document used for payment and customs purposes. If you confuse the two, you risk customs delays, incorrect duty calculations, and documentation disputes.

If you need a dedicated explanation of each document on its own, review our separate guides to commercial invoices and proforma invoices. This page focuses specifically on the commercial invoice vs proforma invoice comparison.

30-Second Quick Answer

Looking for the exact difference? Here is the bottom line:

- Proforma Invoice: A preliminary estimate sent before goods are produced or shipped. According to the U.S. Department of Commerce, it is used for planning, securing financing, and setting expectations, but it holds no legal weight for customs clearance.

- Commercial Invoice: The final, legally binding bill of sale issued after the transaction is confirmed and goods are shipped. It is the primary document used for customs clearance from China to USA because customs uses it to review value, product description, origin, and classification.

- The Core Difference: You usually use a proforma invoice to negotiate and confirm the deal, but customs clearance and final accounting normally rely on the commercial invoice.

Get Your Invoices Reviewed Before Shipping

One missing field can cost you thousands in port fees.

*Reply within 2 hours. No obligation.

Quick Decision: When Do You Use a Proforma Invoice vs a Commercial Invoice?

| Situation | Use Proforma Invoice? | Use Commercial Invoice? |

|---|---|---|

| Price quotation / order approval | Yes | No |

| Opening LC / import planning | Often yes | Sometimes later |

| Final payment support | Sometimes | Usually yes |

| Customs clearance | Rarely as substitute and only in limited cases | Yes |

| Final accounting / tax records | No | Yes |

Core Differences at a Glance

To immediately clarify the functional gaps between these two vital documents, the following table breaks down their characteristics across critical business parameters.

| Feature | Proforma Invoice | Commercial Invoice |

| Primary Purpose | To provide an estimated cost, offer, or sales quote to a potential buyer. | To serve as a legally binding record of the sale and act as an official demand for payment. |

| Timing of Issuance | Issued before the goods are manufactured or shipped. | Issued after the transaction is confirmed and goods are ready. |

| Legal Status | Not legally binding; it is strictly an informational document. | Legally binding and enforceable; represents a finalized contract. |

| Payment Obligation | Does not constitute a formal demand for immediate payment. | Acts as a formal demand for payment based on agreed net terms. |

| Document Flexibility | Highly customizable; terms, quantities, and prices can be revised. | Reflects finalized terms; leaves no room for arbitrary changes. |

| Accounting Role | Not recorded in accounts payable or receivable ledgers. | Mandatory for financial records, cash flow tracking, and taxes. |

| Border Clearance | Rarely accepted for final clearance (used only for pre-clearance). | The mandatory, primary document required for border entry. |

The Document Lifecycle in Global Trade

To understand how these documents govern global trade, it is necessary to isolate their core definitions and identify exactly where they fit within the lifecycle of an international transaction.

Phase 1: Planning and Negotiation (The Proforma)

A proforma invoice is a good-faith estimate issued by the exporter to the buyer. It acts as a highly detailed quotation, outlining the proposed terms of a transaction. Because it is generated during the initial negotiation phase, it is heavily relied upon by buyers to apply for letters of credit from commercial banks, obtain specific government import licenses, and calculate your estimated landed cost.

Phase 2: Execution and Fulfillment (The Logistics)

Once the proforma is signed, production begins. When goods are completed, the focus shifts to physical logistics. During this phase, logistical decisions are made, such as selecting container sizes like 20GP or 40HQ to optimize freight charges. The packing list is generated to match the physical cargo.

Phase 3: Finalization and Payment (The Commercial Invoice)

Issued only after the sale is finalized and the goods are packaged, the commercial invoice serves as the official record. It is the absolute foundational document of an international transaction. It acts as a formal demand for payment and is the primary document used in the customs clearance process to declare value, assess duties, and support import duty from China to USA calculation when the shipment enters the U.S. market.

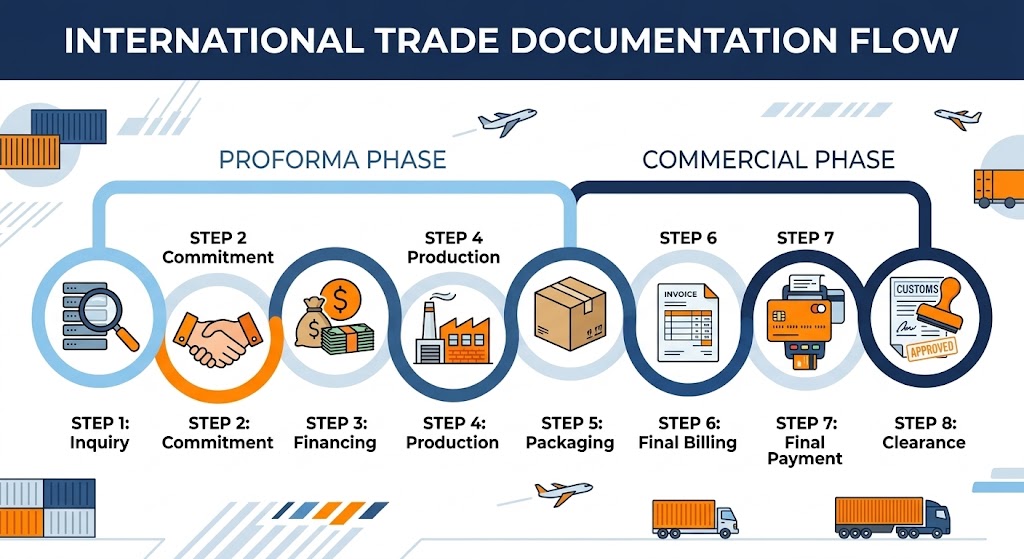

Step-by-Step Workflow Table

| Process Step | Action Performed | Document Used | Responsible Party |

|---|---|---|---|

| 1. Inquiry | Buyer asks for pricing | Quotation | Buyer |

| 2. Commitment | Price agreed, buyer signs | Proforma Invoice | Buyer + Seller |

| 3. Financing | Buyer wires deposit | Proforma Invoice | Buyer |

| 4. Production | Goods manufactured | None | Seller |

| 5. Packaging | Weights/dims recorded | Packing List | Seller |

| 6. Final Billing | Supplier bills final quantities | Commercial Invoice | Seller |

| 7. Final Payment | Buyer wires remaining balance | Commercial Invoice | Buyer |

| 8. Clearance | Broker files entry | Commercial Invoice | Broker |

Specific Requirements for North American Importers

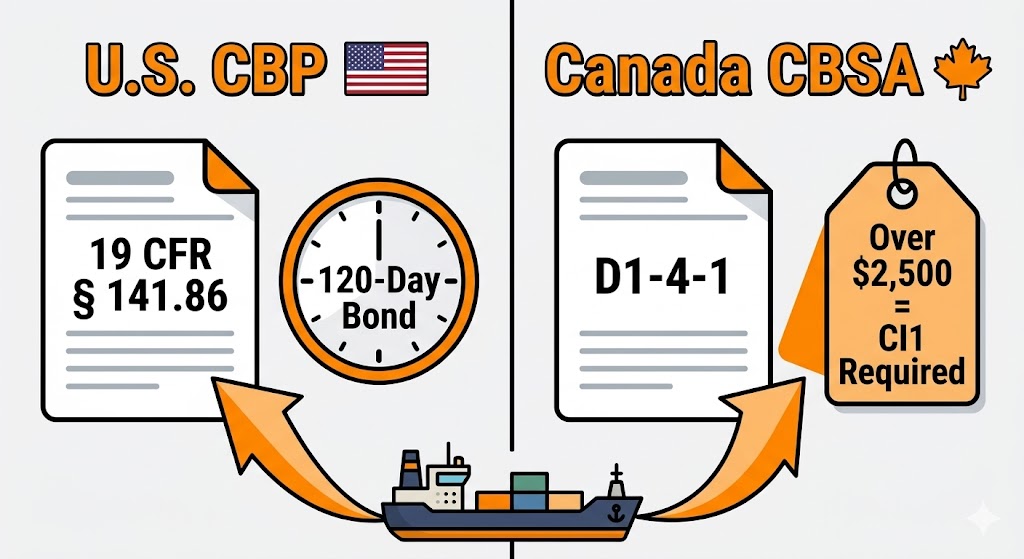

For goods entering the United States, U.S. Customs and Border Protection dictates commercial invoicing standards under 19 CFR § 141.86. The regulation demands detailed information to support tariff appraisement, classification review, and customs entry processing.

U.S. Customs Invoicing Requirements

For goods entering the United States, U.S. Customs and Border Protection (CBP) dictates commercial invoicing standards under 19 CFR § 141.86. The regulation demands exhaustive detail to ensure fair tariff appraisement.

Mandatory CBP Data Elements Table

| Required Data | Detailed Explanation |

| Transaction Parties | Complete names and physical addresses of the seller, buyer, shipper, and receiver. |

| Product Description | Plain-language description sufficient to determine its Harmonized Tariff Schedule (HTSUS) classification. |

| Exact Quantities | Quantities displayed in standard weights and measures (e.g., kilograms, pieces). |

| Financial Values | Unit purchase price and total transaction value, explicitly stating the currency. |

| Logistical Charges | Separate itemization of freight charges, insurance, and packing costs. |

| Origin Details | The specific country where the product was originally manufactured. |

| Assists & Discounts | Value of any molds/tools furnished by the buyer, and all applied trade discounts. |

The 120-Day Proforma Exception (U.S.)

If a required commercial invoice is not available in proper form at the time of entry, CBP may accept the filing only under specific conditions, including a customs bond for production of the correct invoice. In that case, the required invoice generally must be produced within 120 days, or within 50 days when needed for statistical purposes unless an extension is granted.

Canadian Customs Invoicing Requirements

The Canada Border Services Agency (CBSA) maintains its own strict regulations under Memorandum D1-4-1. For Canada, importers generally need a compliant commercial invoice or a CI1-equivalent document containing the required customs data. If the supplier’s invoice does not contain the required information, the importer may need to complete a Canada Customs Invoice (CI1) or provide equivalent data.

Mandatory CBSA Data Elements Table

| Required Data | Detailed Explanation |

|---|---|

| Vendor & Purchaser | Complete legal names and physical addresses. |

| Condition of Sale | Must clearly state delivery and payment terms, such as Incoterms (e.g., FOB, CIF, EXW). |

| Currency of Settlement | The exact currency used for the demand of payment (e.g., USD, CAD). |

| Detailed Specifications | Descriptive marks on packages, accurate descriptions, and HS codes. |

| Origin Data | The specific country of origin where the goods were significantly transformed. |

Canadian Tax Recovery (GST/HST)

The commercial invoice is intrinsically linked to federal tax compliance with the Canada Revenue Agency (CRA). To ensure imports are taxed correctly, a 5% Goods and Services Tax (GST) is collected at the border. Under the new CARM (CBSA Assessment and Revenue Management) initiative, the digital Commercial Accounting Declaration (CAD) replaces the old B3 form. Importers must use finalized commercial invoice data within CARM to legally claim Input Tax Credits (ITCs) for the GST paid at the border. Using proforma estimates for tax filings will result in audit penalties.

Common Costly Mistakes and How to Avoid Them

Because invoices serve as the primary dataset for border officers, simple documentation errors are the leading cause of supply chain delays between Asia, the US, and Canada.

Troubleshooting Border Delays Table

| Common Mistake | Operational Consequence | Recommended Solution |

|---|---|---|

| Using Proforma for Entry | Triggers border rejections. Forces U.S. importers into risky 120-day bond agreements. | Demand the final commercial invoice be transmitted electronically before freight departs. |

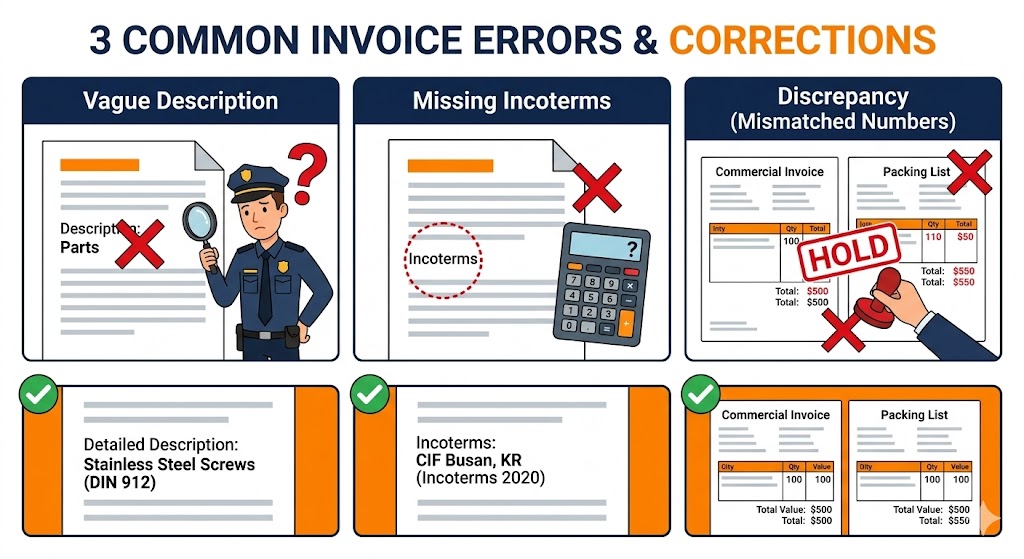

| Vague Descriptions | Terms like “parts” or “accessories” prevent HS code verification, causing physical cargo holds. | Mandate suppliers use plain-language descriptions that align perfectly with tariff schedules. |

| Missing Incoterms | Obscures who paid for freight, altering the dutiable value calculation and risking tax audits. | Provide suppliers with standardized templates that require exact Incoterms (e.g., FOB Shanghai). |

| Data Discrepancies | Mismatched piece counts between the invoice and the Bill of Lading triggers fraud suspicions. | Implement strict three-way matching (PO, Invoice, BOL) before documents are submitted to brokers. |

| Undeclared “Assists” | Failing to list the value of molds or tools provided to the factory illegally lowers entered value. | Ensure purchasing teams communicate with compliance teams when supplying foreign vendors with materials. |

Before the shipment leaves the factory, send the commercial invoice, proforma invoice, packing list, cargo details, supplier address, and destination address together when requesting a shipping quote from China to USA. This helps the forwarder check whether the logistics scope and customs document data are aligned.

Conclusion

By understanding the rigid differences between a proforma and a commercial invoice, standardizing templates, and strictly enforcing documentation rules with foreign suppliers, North American importers can eliminate unnecessary border holds and maintain a highly compliant, predictable supply chain. If you’re not sure whether your supplier’s invoice meets CBP or CBSA standards, have it reviewed before the goods leave the factory—one missing field can cost you thousands in port storage fees.

Whether you are a first-time importer or managing a complex supply chain across multiple countries, the rule never changes: the commercial invoice must be accurate, complete, and compliant with the specific regulations of the destination country. Get it right the first time, and your goods keep moving.

Don’t Let a Bad Invoice Delay Your Cargo

Send us your supplier’s draft Proforma or Commercial Invoice. We’ll verify HS codes, Incoterms, and compliance with CBP and CBSA standards.

*We’ll respond within 2 hours with a compliance report.